Mortgage Broker in Burnaby, BC

Based in Burnaby. Independent. No bank allegiance, no pressure.

Just thorough mortgage advice and someone who sees your file through from start to finish.

⭐⭐⭐⭐⭐ Rated 5 stars by 45 clients on Google

A Simpler Way to Get Your Mortgage Done

Tell Me What You Need

Every mortgage situation is different. Reach out directly and I'll listen first — no pressure to apply before you have answers, no forms to fill out before you're ready. Just a straightforward conversation about where you are and where you want to go.

See Your Real Options

Most people go to their bank and get one set of options. I work with a wide range of lenders and present the options that actually make sense for your situation — with clear explanations of the differences so you can make a confident decision.

Close With Confidence

I handle the paperwork, the lender negotiations, and the follow-up so you can focus on everything else. You'll know exactly where your file stands at every stage — no surprises, no chasing for updates.

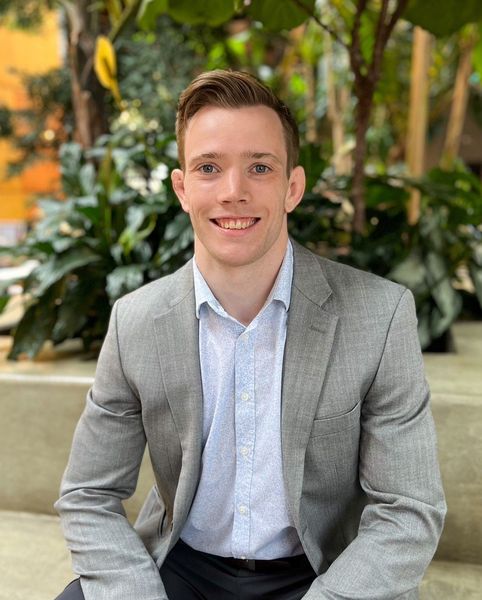

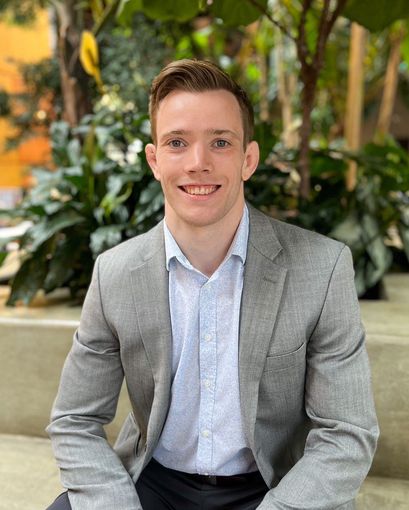

Independent Advice From

Someone Who Does the Work

Before I became a mortgage broker, I graduated from the University of Victoria with a Bachelor of Engineering in Mechanical Engineering and spent five years in technical sales — solving complex problems and explaining them clearly to real people under real pressure.

That's exactly how I approach every mortgage file. I'm analytical where it counts — running numbers across multiple lenders, stress-testing scenarios, identifying the option that saves you the most money over time. And I'm straightforward about how I communicate it, so you understand exactly what you're signing and why.

I work with borrowers across Burnaby, Metro Vancouver, and BC on every type of mortgage situation, first time purchases, renewals, refinances, self-employed applications, investment properties, new to Canada programs, and private lending. If it involves a mortgage, I can help.

Outside of work, I'm a competitive grappler, I've coached and competed at a black belt level in judo and I'm currently training Brazilian jiu-jitsu. I bring that same focus and work ethic to every client file.

My services are free to you in most cases. The lender pays my fee when your mortgage funds. (OAC)

Nice things people have said about working with me.

Why Work With Me Instead of Going to Your Bank?

When you go to your bank, you see that bank's products at that bank's rates. When you work with me, you get access to a wide range of lenders competing for your business — and someone in your corner whose only job is to find you the best one.

Here's what that means in practice:

Get started by completing my online mortgage application.

When it comes to getting the financial service you deserve, don't settle for slow, limited options and poor treatment – choose a mortgage broker who puts you first.

Let's run some numbers.

Mortgage Services in Burnaby, BC

Whatever your situation, I have the lender relationships and product knowledge to find the right solution.

Click through any of the services to learn more

- First Time Home Buyers — I'll walk you through every step, pre-approval, programs, down payment options, and closing, so you buy with confidence, not anxiety.

- Home Purchase — Buying your next property in Metro Vancouver? I'll shop the market and find you the best purchase mortgage available for your file.

- Mortgage Refinance — Want to access your equity, consolidate debt, or lower your rate? I'll model the numbers so you know whether it makes financial sense before you commit to anything.

- Mortgage Renewal — Don't just sign what your lender sends you. I'll compare your renewal offer against the full market so you always know if there's a better deal available.

- Self-Employed — Business write-offs reducing your declared income? I have access to lenders who look at your file differently and give you full credit for what you actually earn.

- New to Canada — Permanent resident, work permit holder, or newcomer? I work with programs from CMHC, Sagen, and Canada Guaranty designed specifically for your situation.

- Investment Properties — Building a portfolio? I understand how rental income is calculated across lenders and structure your application to maximize your qualifying power.

- Private Lending — When traditional lenders aren't the right fit, I have access to private and alternative lending solutions for short-term needs.

Ready to Find Your Best Mortgage?

Mortgage articles to keep you informed.

Frequently Asked Questions

What does a mortgage broker do?

I act as the intermediary between you and mortgage lenders. Instead of you going to each lender individually, I compare rates and products across a wide range of lenders on your behalf — finding the best fit for your specific situation. I handle the application, the paperwork, and the lender communication from start to finish.

Is it free to use a mortgage broker in BC?

In most cases, yes — completely free to you. I'm compensated by the lender when your mortgage funds, not by you. That means you get access to my full service — lender shopping, rate comparison, application management, and ongoing advice — at no direct cost. There are some situations involving private or alternative lenders where a broker fee applies, and I'll always be upfront about that before we proceed.

What's the difference between a mortgage broker and a bank?

When you go to your bank, you see that bank's products at that bank's rates. When you work with me, I have access to a wide range of lenders — major banks, credit unions, trust companies, and private lenders — and I compare them all to find you the best fit. I work for you, not for any single lender. That's the fundamental difference.

How do I qualify for a mortgage in Canada?

Lenders look at three primary things: your income (to confirm you can afford the payments), your credit history (to assess how reliably you manage debt), and your down payment (minimum 5% for purchases under $500,000). Every application also goes through the federal mortgage stress test, which qualifies you at your contract rate plus 2%, or 5.25% — whichever is higher. I review all three with you upfront so you know exactly where you stand before we submit anything.

What credit score do I need to get a mortgage in BC?

Most lenders require a minimum credit score of 620–680 for insured mortgages. The higher your score, the more lender options you have and the better rates you'll access. If your score isn't where it needs to be yet, I'll tell you exactly what's affecting it and give you a clear plan to improve it before you apply. I'd rather help you get it right the first time than have a declined application on your record.

How long does mortgage approval take in Canada?

A pre-approval can typically be completed within 24–72 hours. Full mortgage approval after an accepted offer usually takes 5–10 business days depending on the lender and the complexity of your file. I manage the entire process and keep you updated at every stage — you'll never be left wondering where things stand or chasing me for an update.

Can I get a mortgage if I'm self-employed in BC?

Yes. Self-employment doesn't disqualify you — but it does mean lender selection matters much more for your file than it does for a salaried borrower. I specialize in self-employed mortgages and I have access to both traditional lenders with flexible income programs and alternative lenders who look at your gross revenue or bank deposits rather than just your net declared income. Reach out and I'll give you an honest picture of your options.